What If The Fed Has It All Wrong?: I wrote an exclusive article for Seeking Alpha in which I expand on the following points:

Quantitative Easing-induced wealth effects may be wishful thinking;

Earnings are the primary drivers for equities and they have peaked;

QE3 could be highly counterproductive if commodity prices [...]

Tuesday, September 25, 2012

Tuesday, September 11, 2012

Tuesday, September 04, 2012

Who Do You Blame for the Woes of the Middle-Class?

Who Do You Blame for the Woes of the Middle-Class?: The Pew Research center ponders The Lost Decade of the Middle Class.

Median net worth is back to a level first seen in the 1980s. By that measure, the US has had three lost decades. Wow.

62% Blame Politicians, Only 8% Blame Themselves

Note that 62% blame politicians and 54% blame financial institutions, but only 8% blame themselves.

Five Questions

Two Bonus Questions

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Since 2000, the middle class has shrunk in size, fallen backward in income and wealth, and shed some—but by no means all—of its characteristic faith in the future.Three Lost Decades!

These stark assessments are based on findings from a new nationally representative Pew Research Center survey that includes 1,287 adults who describe themselves as middle class, supplemented by the Center’s analysis of data from the U.S. Census Bureau and Federal Reserve Board of Governors.

Median Income

Median Net Worth

Fully 85% of self-described middle-class adults say it is more difficult now than it was a decade ago for middle-class people to maintain their standard of living. Of those who feel this way, 62% say “a lot” of the blame lies with Congress, while 54% say the same about banks and financial institutions, 47% about large corporations, 44% about the Bush administration, 39% about foreign competition and 34% about the Obama administration. Just 8% blame the middle class itself a lot.

Who Is To Blame?

Median net worth is back to a level first seen in the 1980s. By that measure, the US has had three lost decades. Wow.

62% Blame Politicians, Only 8% Blame Themselves

Note that 62% blame politicians and 54% blame financial institutions, but only 8% blame themselves.

Five Questions

- Did banks force people to take out loans they could not pay back, or did people do so voluntarily?

- Who elects congress?

- Do people make enough effort to understand interest rates, debt, the economic policies of politicians, exponential math and its implications, the untenable nature of public union pension plans and promises?

- Do a significant number of people (if not the majority) get their economic views (assuming they have any economic views) from The View, Oprah, The Talk, or CNBC?

- Why did PEW leave off the Fed and Fractional Reserve Lending from the list of answers?

Two Bonus Questions

- Would the majority of respondents know anything at all about the Fed and Fractional Reserve lending had the PEW listed those options?

- Who is really to blame for what is happening?

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

Saturday, September 01, 2012

Volatility Analogy

Volatility Analogy:

Today Heidi Moore interviewed me for NPR Marketplace. I won’t give away what it is about, but I will tell you two things:

Imagine you are driving down a well-engineered smooth road with gradual turns, modest traffic, and no bad weather, and you are going 60 miles per hour. This is easy. There is no volatility here. That is what an average retail investor hopes for, and rarely gets.

Now consider a road that is not so smooth, with significant and frequent curves, significant traffic, and now and then it is raining hard. That is a difficult situation. This is similar to what the market is normally like, with all of the volatility (high variation of results). Maybe you can’t do 60 MPH in that environment, but something less. Those who recognize risk must run at a slower speed or risk accidents.

Now think of someone without special skills who dares to drive the easy road at 100 MPH. He might not think it so hard, and might think he is quite a driver doing so. So it was for equity investors in the ’80s and ’90s; conditions were uniquely favorable, and average investors thought they were hot stuff.

Now think of someone without special skills attempting to do the hard conditions at 100 MPH on average. Odds are they wipe out, or even die. You can’t fight physics, or can you?

Okay, now think of a highly trained driver with a special car that is able to handle the hard conditions, and can do it at 100 MPH on average, most of the time. It doesn’t work all of the time, because there are things no one can catch — extra slipperiness, a bump in a particularly bad place that leads to an overturned car.

Finally, think of the trained driver with special car told he must average 150 MPH over the hard conditions course once. He dies on the first try, destroying the car. Several other trained drivers try with identical cars. They all die, and the cars are destroyed. Eventually, you can’t get anyone to try the hard conditions course at 150 MPH.

-=-=-=-==–=-=-==–=-=-=-=-=-=-=-=-=-=-=-=-=-=-=

In my analogy, the difference between the hard and easy course is volatility: how rough/variable are conditions. Leverage is represented by speed. Any course can be completed, but there is a maximum speed for which a course can be completed without disaster. No surprise that those who are overly aggressive in investing frequently fail.

Now for the final tweak: imagine that you have no map for the hard course, it is new to you, no GPS, nothing to aid you in the driving. That is what the markets are like. As I often say, the markets always have a new way to make a fool out of you. How fast could you go? How fast could the trained driver with a special car go?

This is why I urge caution in investing and avoiding leverage. Investing is tough enough without trying to earn something beyond what the market can bear. I encourage safety first, after that, look for best advantage.

Today Heidi Moore interviewed me for NPR Marketplace. I won’t give away what it is about, but I will tell you two things:

- If I am on Marketplace, it will be on Friday or Tuesday.

- There was a point in the interview where she stumped me. I’m usually pretty able to think on my feet, but when she asked me “Volatilty: can you explain that in language that a teenager could understand?” I choked up, did my best on short notice, and gave what I later viewed as a lame explanation, but as I said it, my heart sank, because I realized I was not clarifying anything.

Imagine you are driving down a well-engineered smooth road with gradual turns, modest traffic, and no bad weather, and you are going 60 miles per hour. This is easy. There is no volatility here. That is what an average retail investor hopes for, and rarely gets.

Now consider a road that is not so smooth, with significant and frequent curves, significant traffic, and now and then it is raining hard. That is a difficult situation. This is similar to what the market is normally like, with all of the volatility (high variation of results). Maybe you can’t do 60 MPH in that environment, but something less. Those who recognize risk must run at a slower speed or risk accidents.

Now think of someone without special skills who dares to drive the easy road at 100 MPH. He might not think it so hard, and might think he is quite a driver doing so. So it was for equity investors in the ’80s and ’90s; conditions were uniquely favorable, and average investors thought they were hot stuff.

Now think of someone without special skills attempting to do the hard conditions at 100 MPH on average. Odds are they wipe out, or even die. You can’t fight physics, or can you?

Okay, now think of a highly trained driver with a special car that is able to handle the hard conditions, and can do it at 100 MPH on average, most of the time. It doesn’t work all of the time, because there are things no one can catch — extra slipperiness, a bump in a particularly bad place that leads to an overturned car.

Finally, think of the trained driver with special car told he must average 150 MPH over the hard conditions course once. He dies on the first try, destroying the car. Several other trained drivers try with identical cars. They all die, and the cars are destroyed. Eventually, you can’t get anyone to try the hard conditions course at 150 MPH.

-=-=-=-==–=-=-==–=-=-=-=-=-=-=-=-=-=-=-=-=-=-=

In my analogy, the difference between the hard and easy course is volatility: how rough/variable are conditions. Leverage is represented by speed. Any course can be completed, but there is a maximum speed for which a course can be completed without disaster. No surprise that those who are overly aggressive in investing frequently fail.

Now for the final tweak: imagine that you have no map for the hard course, it is new to you, no GPS, nothing to aid you in the driving. That is what the markets are like. As I often say, the markets always have a new way to make a fool out of you. How fast could you go? How fast could the trained driver with a special car go?

This is why I urge caution in investing and avoiding leverage. Investing is tough enough without trying to earn something beyond what the market can bear. I encourage safety first, after that, look for best advantage.

Sunday, August 26, 2012

How Warren Buffett is Different from Most Investors, Part 1

How Warren Buffett is Different from Most Investors, Part 1:

There was an academic article published recently on the investing of Warren Buffett. Afterward, I thought I saw a few articles reflecting on it, but here is the only one I see now: There’s Warren Buffett — and then there’s the rest of us.

Buffett is different, because he grew as an investor and as a businessman, and usually made the right moves over a 50+ year career. When you don’t have a lot of assets, and few people are doing value investing, you can do amazing things with special situations, and being an activist investor. In 1967, Buffett had control of a textile company named Berkshire Hathaway, when he used the resources of the company to purchase some smallish P&C insurance companies, National Indemnity and National Fire and Marine Insurance.

This brings up the first way that Buffett is different than most investors. He understands and invests in a complex industry, P&C insurance. He begins to realize that it can be used as a platform for greater investing. As he sees that potential, he buys half of GEICO in the 70s, before buying the whole company in 1994.

This brings up the second way that Buffett is different than most investors: Buffett was willing to buy whole companies, not replace management for the most part, and operate them. Buffett limited himself to being the wholly-owned company’s board, asking questions on management competence, and redirecting free cash flow for the greater good of Berkshire Hathaway.

That brings me to the third way in which Buffett is different than most investors: He analyzes cash flow streams from investments, and buys shares in companies, or the whole company when they offer a reliable high prospective free cash flow yield. And it brings me to the fourth way Warren Buffett is different than most investors: Buffett does not diversify, particularly in the early years. He plays for best advantage. Buffett views investing through the lens of compounding cash flows, and does not pay much attention to the market as a whole.

In my opinion, it is a worthy use of time (but don’t neglect your family) to read through the annual letters of Berkshire Hathaway. If you do that, you will get a sense of a clever businessman who would invest for best advantage. His tactics shifted over time, but he was always looking to compound free cash flows at the best possible rate.

I’m going to hit the publish button now, but I will finish this in part 2.

There was an academic article published recently on the investing of Warren Buffett. Afterward, I thought I saw a few articles reflecting on it, but here is the only one I see now: There’s Warren Buffett — and then there’s the rest of us.

Buffett is different, because he grew as an investor and as a businessman, and usually made the right moves over a 50+ year career. When you don’t have a lot of assets, and few people are doing value investing, you can do amazing things with special situations, and being an activist investor. In 1967, Buffett had control of a textile company named Berkshire Hathaway, when he used the resources of the company to purchase some smallish P&C insurance companies, National Indemnity and National Fire and Marine Insurance.

This brings up the first way that Buffett is different than most investors. He understands and invests in a complex industry, P&C insurance. He begins to realize that it can be used as a platform for greater investing. As he sees that potential, he buys half of GEICO in the 70s, before buying the whole company in 1994.

This brings up the second way that Buffett is different than most investors: Buffett was willing to buy whole companies, not replace management for the most part, and operate them. Buffett limited himself to being the wholly-owned company’s board, asking questions on management competence, and redirecting free cash flow for the greater good of Berkshire Hathaway.

That brings me to the third way in which Buffett is different than most investors: He analyzes cash flow streams from investments, and buys shares in companies, or the whole company when they offer a reliable high prospective free cash flow yield. And it brings me to the fourth way Warren Buffett is different than most investors: Buffett does not diversify, particularly in the early years. He plays for best advantage. Buffett views investing through the lens of compounding cash flows, and does not pay much attention to the market as a whole.

In my opinion, it is a worthy use of time (but don’t neglect your family) to read through the annual letters of Berkshire Hathaway. If you do that, you will get a sense of a clever businessman who would invest for best advantage. His tactics shifted over time, but he was always looking to compound free cash flows at the best possible rate.

I’m going to hit the publish button now, but I will finish this in part 2.

Saturday, August 18, 2012

The Slowing De-leveraging….

The Slowing De-leveraging….:

I’ve long predicted that the balance sheet recession was likely to come to an end somewhere around 2013/2014 and it looks like the de-leveraging process in the USA has certainly slowed. This excellent chart from Morgan Stanley (via Joe W) shows how the de-leveraging has improved over the years. Unfortunately, we’re not quite at a point where the public sector can hand off the baton yet. We still have some work to do so we’re likely looking at something closer to a 2014 hand-off of the baton. Of course, that’s assuming the fiscal cliff doesn’t torpedo the private sector recovery right when it looks like it’s starting to catch its footing….

I’ve long predicted that the balance sheet recession was likely to come to an end somewhere around 2013/2014 and it looks like the de-leveraging process in the USA has certainly slowed. This excellent chart from Morgan Stanley (via Joe W) shows how the de-leveraging has improved over the years. Unfortunately, we’re not quite at a point where the public sector can hand off the baton yet. We still have some work to do so we’re likely looking at something closer to a 2014 hand-off of the baton. Of course, that’s assuming the fiscal cliff doesn’t torpedo the private sector recovery right when it looks like it’s starting to catch its footing….

Source: Morgan Stanley via Joe Weisenthal

Monday, August 13, 2012

Gary Shilling: US in Recession Now or Within 3 Months, Deleveraging Will Take 5-7 More Years

Gary Shilling: US in Recession Now or Within 3 Months, Deleveraging Will Take 5-7 More Years: In a Daily Ticker Interview with Henry Blodget, economist Gary Shilling makes the case the US is already in recession.

On June 21, I made the case 12 Reasons US Recession Has Arrived (Or Will Shortly)

On July 11, I wrote Case for US and Global Recession Right Here, Right Now; Recognizing the Limits of Madness; Permabears?

More QE is Pointless

While everyone is looking for another round of QE, on August 1, I explained Another Round of QE is Pointless.

Shilling thinks the recession started in the second quarter. Obviously, I agree.

It will be interesting to see when and where the NBER places it.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

"We've had three consecutive months of declines in retail sales," says Shilling, president of A. Shilling & Co., an economic research and forecasting firm. "That's happened 29 times since they started collecting the data in 1947, and in 27 of the 29 we were either in a recession or within three months of it."Case for Recession

Shilling expects this recession will last about a year and shave about 3.5% from growth from peak to trough.

This time is different, says Shilling "because a lot of things that normally go down in a recession are already there, like housing." And policies that normally help revive the economy are absent. The Fed can't cut interest rates because they're already near zero and the housing market won't be a catalyst for growth, Shilling says.

Before the last presidential election Shilling said that whoever got elected then wouldn't get re-elected because the economy would still be weak with high unemployment.

Now Shilling says he'd like to see one party in control in Washington because it increases the odds of cuts for entitlements and could help "restore confidence in Washington." But even then he says it will take five to seven years to complete the deleveraging that's already underway before the economy recovers.

On June 21, I made the case 12 Reasons US Recession Has Arrived (Or Will Shortly)

On July 11, I wrote Case for US and Global Recession Right Here, Right Now; Recognizing the Limits of Madness; Permabears?

More QE is Pointless

While everyone is looking for another round of QE, on August 1, I explained Another Round of QE is Pointless.

Would Another Round of QE Help?Timing the Recession

Everyone is looking for the Fed to do something.

I have to ask what good could it possibly do? Yield on the 10-year

treasury is about 1.5%. Would it make any difference to businesses if it

was 1.25% or even 1%?

I suggest additional monetary stimulus would not do anything to spur job

creation and it would continue to punish those on fixed incomes.

An additional round of QE could ignite a further rally in equities

(already in bubble land). However, one of these QE moves by the Fed will

blow sky high, and with equities priced beyond perfection, the next

round of QE may be the one.

Shilling thinks the recession started in the second quarter. Obviously, I agree.

It will be interesting to see when and where the NBER places it.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

Tuesday, August 07, 2012

Guest Post: While All Eyes Are On Europe, Japan Circles A Black Hole

Guest Post: While All Eyes Are On Europe, Japan Circles A Black Hole:

Submitted by Charles Hugh-Smith of OfTwoMinds blog,

While all eyes are on the absurdist tragicomedy playing out in Europe, Japan is quietly circling a financial black hole as its export economy is destroyed by its strong currency and the global recession.

There is a terrible irony in export-dependent nations being viewed as "safe havens." Their safe haven status pushes their currencies higher, which then crushes their export sector, which then weakens their entire economy and stability, undermining the very factors that created their safe haven status.

As long as Germany stays within the Eurozone, Japan is the primary example of this dynamic. Should Germany leave the euro and return to its own currency, it too will begin orbiting the financial black hole of declining exports driven by a strengthening currency in a global recession.

Economies that are less reliant on exports are much less exposed to the consequences of a strengthening currency.

We can lay out the dynamic of Japan's currency and export-dependent economy thusly:

1. Export-dependent economies such as Japan, China and Germany rely on strong exports to sustain their employment and growth.

2. This means they must maintain positive current accounts (trade surpluses).

3. As their currencies strengthen, their exports become less competitive globally.

4. Export-dependent economies must pursue strategies to keep their currencies aligned with their buyers, the importing nations.

5. Germany has done so via the eurozone, which aligned its largest import market, Europe, with its own currency.

6. China has done so by pegging the renminbi (yuan) to the U.S. dollar and restricting foreign exchange (i.e. not allowing a free-floating renminbi).

7. Japan has neither of these advantages, and must intervene in the FX markets by buying and selling yen and dollars.

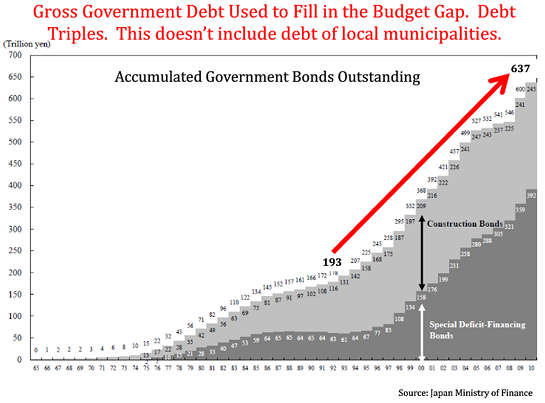

8. Despite its well-known debt problems (see chart below), Japan retains a massive and diverse industrial base, a current-account surplus (or modest deficit with its nuclear power plants largely offline) and large overseas assets.

9. These assets, plus its homogeneous culture, makes Japan an island of stability in an increasingly unstable global economy.

10. For these reasons, the yen is considered a "safe haven" currency and yen-denominated bonds as "safe haven" liquid investments.

11. As demand for yen rises, the currency strengthens, weakening the competitiveness of Japanese exports.

12. The "safe haven" status of the yen ends up hurting the Japanese economy's primary engine, exports.

13. The stronger yen ends up weakening the very attributes that make the yen and Japanese bonds "safe havens."

14. As the global economy slides into recession, exports decline sharply under the double-whammy of falling demand and a rising currency.

Ironic, to say the least.

Submitted by Charles Hugh-Smith of OfTwoMinds blog,

While all eyes are on the absurdist tragicomedy playing out in Europe, Japan is quietly circling a financial black hole as its export economy is destroyed by its strong currency and the global recession.

There is a terrible irony in export-dependent nations being viewed as "safe havens." Their safe haven status pushes their currencies higher, which then crushes their export sector, which then weakens their entire economy and stability, undermining the very factors that created their safe haven status.

As long as Germany stays within the Eurozone, Japan is the primary example of this dynamic. Should Germany leave the euro and return to its own currency, it too will begin orbiting the financial black hole of declining exports driven by a strengthening currency in a global recession.

Economies that are less reliant on exports are much less exposed to the consequences of a strengthening currency.

We can lay out the dynamic of Japan's currency and export-dependent economy thusly:

1. Export-dependent economies such as Japan, China and Germany rely on strong exports to sustain their employment and growth.

2. This means they must maintain positive current accounts (trade surpluses).

3. As their currencies strengthen, their exports become less competitive globally.

4. Export-dependent economies must pursue strategies to keep their currencies aligned with their buyers, the importing nations.

5. Germany has done so via the eurozone, which aligned its largest import market, Europe, with its own currency.

6. China has done so by pegging the renminbi (yuan) to the U.S. dollar and restricting foreign exchange (i.e. not allowing a free-floating renminbi).

7. Japan has neither of these advantages, and must intervene in the FX markets by buying and selling yen and dollars.

8. Despite its well-known debt problems (see chart below), Japan retains a massive and diverse industrial base, a current-account surplus (or modest deficit with its nuclear power plants largely offline) and large overseas assets.

9. These assets, plus its homogeneous culture, makes Japan an island of stability in an increasingly unstable global economy.

10. For these reasons, the yen is considered a "safe haven" currency and yen-denominated bonds as "safe haven" liquid investments.

11. As demand for yen rises, the currency strengthens, weakening the competitiveness of Japanese exports.

12. The "safe haven" status of the yen ends up hurting the Japanese economy's primary engine, exports.

13. The stronger yen ends up weakening the very attributes that make the yen and Japanese bonds "safe havens."

14. As the global economy slides into recession, exports decline sharply under the double-whammy of falling demand and a rising currency.

Ironic, to say the least.

Monday, July 30, 2012

The Market Ticker - Capital Account with Doug Casey

The Market Ticker - Capital Account with Doug Casey:

More good financial journalism -- another "must see" from the fine folks at Capital Account.

https://www.youtube.com/watch?v=fbyF_17GTNA

More good financial journalism -- another "must see" from the fine folks at Capital Account.

https://www.youtube.com/watch?v=fbyF_17GTNA

Sunday, July 29, 2012

How Much More Does The Bear Market Have To Go?

How Much More Does The Bear Market Have To Go?:

The secular bear market that the US has been caught in for a better part of the last decade will end. Eventually. The only question is when. Last week we reported that the bulk of market gains year to date, has been driven exclusively by PE multiple expansion, which is to be expected: EPS forecasts for the end of 2012 are now the lowest they have been since the beginning of the year. Yet while such sharp, sudden and short and bear-market rallies, exclusively on the back of the global central banks, are to be expected, the bigger question is how much more of a secular decline in PE multiples is to be expected before the bear market ends and a new bull market can begin. As the following chart from Crestmont Research shows there is quite a bit more to go, even with Fed assistance (or rather, because of it, and its forced rejection of reaching a fair clearing price sooner rather than later), before the bear market is officially over. Just over 50% more. To the downside.

How the Bear Market declines have looked in perspective, and where we ultimately have to go before all the artifical supports are cleared out:

And the Bull Markets preceding them...

h/t Things That Make you go Hmmm

The secular bear market that the US has been caught in for a better part of the last decade will end. Eventually. The only question is when. Last week we reported that the bulk of market gains year to date, has been driven exclusively by PE multiple expansion, which is to be expected: EPS forecasts for the end of 2012 are now the lowest they have been since the beginning of the year. Yet while such sharp, sudden and short and bear-market rallies, exclusively on the back of the global central banks, are to be expected, the bigger question is how much more of a secular decline in PE multiples is to be expected before the bear market ends and a new bull market can begin. As the following chart from Crestmont Research shows there is quite a bit more to go, even with Fed assistance (or rather, because of it, and its forced rejection of reaching a fair clearing price sooner rather than later), before the bear market is officially over. Just over 50% more. To the downside.

How the Bear Market declines have looked in perspective, and where we ultimately have to go before all the artifical supports are cleared out:

And the Bull Markets preceding them...

h/t Things That Make you go Hmmm

Thursday, July 26, 2012

Kyle Bass Vindication Imminent? Largest Japanese Pension Fund Begins To Sell JGBs

Kyle Bass Vindication Imminent? Largest Japanese Pension Fund Begins To Sell JGBs:

Sayonara internal funding. In what we suspect will become a major issue (and warned in April of last year), Bloomberg reports that Japan’s public pension fund, the world’s largest, said it has been selling domestic government bonds as the number of people eligible for retirement payments increases. "Payouts are getting bigger than insurance revenue, so we need to sell Japanese government bonds to raise cash." It would appear the Ponzi has reached it's Tipping Point. Japan’s population is aging, and baby boomers born in the wake of World War II are beginning to reach 65 and eligible for pensions. That’s putting GPIF under pressure to sell JGBs so it can cover the increase in payouts.

The fund needs to raise about 8.87 trillion yen this fiscal year. GPIF is historically one of the biggest buyers of Japanese debt and held 71.9 trillion yen, or 63 percent of its assets, in domestic bonds as of March.

This leaves the biggest question "to whom will the pension fund sell?" After all it is all marginal and everyone just front-runs the biggest players (Governments and their Central-Bank caring internal funds). Now that the pensions funds are out, there is no more incentive to frontrun them - a la The Fed - which is summed up by the fund's manager "There isn’t much value in short-term notes as the BOJ’s massive asset purchases have made their yields extremely low."

From our April 2011 thoughts:

and from SocGen's Dylan Grice 2010 views (full presentation here):

And As Kyle Bass has questioned numerous times, will 2010 be the beginning of the end of flawed Keynesian economics?

Sayonara internal funding. In what we suspect will become a major issue (and warned in April of last year), Bloomberg reports that Japan’s public pension fund, the world’s largest, said it has been selling domestic government bonds as the number of people eligible for retirement payments increases. "Payouts are getting bigger than insurance revenue, so we need to sell Japanese government bonds to raise cash." It would appear the Ponzi has reached it's Tipping Point. Japan’s population is aging, and baby boomers born in the wake of World War II are beginning to reach 65 and eligible for pensions. That’s putting GPIF under pressure to sell JGBs so it can cover the increase in payouts.

The fund needs to raise about 8.87 trillion yen this fiscal year. GPIF is historically one of the biggest buyers of Japanese debt and held 71.9 trillion yen, or 63 percent of its assets, in domestic bonds as of March.

This leaves the biggest question "to whom will the pension fund sell?" After all it is all marginal and everyone just front-runs the biggest players (Governments and their Central-Bank caring internal funds). Now that the pensions funds are out, there is no more incentive to frontrun them - a la The Fed - which is summed up by the fund's manager "There isn’t much value in short-term notes as the BOJ’s massive asset purchases have made their yields extremely low."

From our April 2011 thoughts:

In the world of bonds, few things have perplexed investors as much as the ridiculously low (and going lower) rates of Japanese Government Bonds (JGBs), at last check yielding 1.22%. Granted "deflation" in Japan has long been quoted as the key driver for the ongoing decline in real and nominal rates, but in practical market terms it was always the fact that there was a buyer of first and last resort, usually this being either Japanese citizens directly or their proxy, the Japanese Government Pension Investment Fund (GPIF) that kept yields in check and sliding.

and from SocGen's Dylan Grice 2010 views (full presentation here):

This is far from just a JGB market problem. As Japan's retirees age and run down their wealth, Japan's policymakers will be forced to sell assets, including US Treasuries currently worth $750bn, or Y70 trillion "eight months" worth of domestic financing. At nearly 10% of the outstanding US Treasury stock, this might well precipitate other government funding crises (bearing in mind that the Japanese model is the argument buttressing confidence in Western government bonds in the face of deteriorating fiscal conditions). At the very least I'd expect it to trigger an international bond market rout scary enough to spook all other asset classes.

And As Kyle Bass has questioned numerous times, will 2010 be the beginning of the end of flawed Keynesian economics?

(h/t Brian)Maybe Japan's will be the crisis that wakes up the rest of the world and triggers some tough decisions on world-wide debt loads. Or maybe not - maybe the Greeks will beat them to it? or the Irish or the UK, or the US? Like banks in 2007, developed market governments today rely on sustained capital markets more than any time in their history. What if they shut?

Wednesday, July 25, 2012

David Stockman: "The Capital Markets Are Simply A Branch Casino Of The Central Bank"

David Stockman: "The Capital Markets Are Simply A Branch Casino Of The Central Bank":

A selected excerpt by David Stockman from his just released interview with Alex Daley of Casey Research:

The New Economic Collapse Video: It makes uncomfortable but urgent viewing.

When Casey Research Chief Technology Investment Analyst Alex Daley met former Reagan Budget Director David Stockman to talk about the economy and where he sees it leading taxpayers investors and savers in the near future, he got some very intriguing insights from a man who served right at the heart of the US federal government.

True, some if it makes for uncomfortable watching, but the message is critical if you want to keep your assets safe in what David calls calls "the great unwind."

Watch the video and secure your money.

Full Transcript:

Interviewed by Alex Daley, Chief Technology Investment Strategist, Casey Research

Alex Daley: Hello. I'm Alex Daley. Welcome to another edition of Conversations with Casey. Today our guest is former Reagan Budget Director and Congressman David Stockman. Welcome to the show, David.

David Stockman: Glad to be here.

Alex: So we're here in Florida talking at the Recovery Reality Check Casey Summit. What do you think: is the United States economy on the road to recovery?

David: I don't think we are at the beginning of the recovery. I think we are at the end of a disastrous debt supercycle that has gone on for the last thirty or forty years, really. It started when Nixon defaulted on our obligations under Bretton Woods and closed the gold window. Incrementally, year after year since then, we have been going in a direction of extremely unsound money, of massive borrowing in both the private and the public sector. We now have an economy that is saturated with debt: $54 trillion or $53 trillion – 3.5 times the GDP – way off the charts from where it was for a hundred years prior to the beginning of this. The idea that somehow all of that debt is irrelevant, as the Keynesians would tell us, is fundamentally wrong – and the reason why the economy can't get up off the mat.

We're doing all the wrong things. We're adding to the problem, not subtracting. We are not allowing the debt to be worked down and liquidated. We're not asking people to save more and consume less, which is what we really need to do. And so therefore I think policy is just making it worse, and any day now we will have another recurrence of the kind of economic crisis we had a few years ago.

Alex: You paint a very stark picture, but if people just stop spending, start saving, won't companies like Apple see their earnings hurt? Won't the stock market then start to tumble, people's net worth fall? Isn't that a negative cycle that feeds on itself?

David: Sure it does, but you can't live beyond your means because it's pleasant. It's not sustainable. Clearly the level of debt that we have is not sustainable. We have a whole generation – the Baby Boom – that's about ready to retire, and they have no retirement savings. We have a federal government that is bankrupt, literally. Its [debt is] $16 trillion and growing by a trillion a year. Something's going to give. We can't pay for all these entitlements. There won't be the revenue generation in the economy to do it.

So as a result of that, we are deluding ourselves if we think we can just continue to spend. Look at the GDP that came out in the first quarter of this year. It was only 2.2%. Most of it was personal consumption expenditure, and half of that was due to a drawdown of the savings rate, not because the economy was earning more income or generating more real output. It was because of a drawdown of savings. That is exactly the wrong way to go – an indication of how severe the crisis is going to be.

I'm not saying the economy should stop spending entirely. I'm only saying you can't save 3% of GDP and spend 97% if you are going to get out of this fix. As the savings rate goes up both in the public sector (which means reduction of spending and the deficit) and the household sector (to seriously reduce debt burden, which has not really happened) we are going to, on the margin, spend less, save more. It will slow down the economy. It will undermine profits, I agree. But profits today are way overstated. They're based on a debt-bloated economy that isn't sustainable.

Alex: So we can only live beyond our means for so long, as any family knows.

David: Yes.

Alex: Now, the government can reduce its expenses at any time by simply reducing spending, and it can reduce debt if it brings in more tax revenue. That's austerity – I think that's how they refer to it. But won't austerity cause massive joblessness? Won't there be millions more people in this country not receiving a paycheck?

David: Yes, but the critique, the clamoring and clattering that you hear from the Keynesians (or even mainstream media, which is pretty clueless economically) that austerity is bad forgets the fact that austerity isn't an elective course. Austerity is something that happens to you when you're broke. And yes, it is painful and spending will go down and unemployment will go up and incomes will be impaired, but that is a consequence of the excess debt creation that we've had for the last thirty years. So austerity is what happens when you break the rules.

And somehow we have this debate going on. They're making a mistake. They chose the wrong strategy. Do you think Greece chose the wrong strategy with austerity? No. No one would lend them money. That's why they ended up in the place they were. Do you think that Spain today is teetering on the brink because they said, "Oh, wouldn't it be a good idea to have austerity?" No, they had a gun to their head. They were forced to do this because the markets would not continue to lend, and even now their interest rate is again rising. The markets are losing confidence, and unless the ECB prints some more money and bails them out some more, they are going to have austerity. So the austerity upon us is the backside of the debt supercycle we had for the past thirty years. It's not discretionary.

Alex: Austerity hasn't been forced upon us yet. The dollar is up, people are continuing to buy Treasuries – both nations and banks are buying Treasuries. To all extents and purposes, people are continuing to show massive confidence in the US government, lend it money at extremely cheap interest rates, and letting it build up its debt.

So you are advocating that, unlike Greece or Spain taking it to the edge and having austerity forced on them, we should volunteer for austerity today? Instead of just kicking the can down the road and living high a little bit longer, until the bill collectors finally come knocking? Why go today, why start austerity now instead of doing what Greece did and going as long as you possibly can?

David: Because Greece is a $300 billion economy. Tiny. A rounding error in the great scheme of things. It's – last time I checked – about eight and a half months' worth of Walmart sales. Okay? That's a little different than when you have the $15 trillion heartland of the world economy, and the $11 trillion Treasury market which is at the center of the whole global financial system buckle and falter. That's the risk you're taking if you say, "Mañana. Kick the can; let's just wait for something good to happen."

This market isn't real. The two percent on the ten-year, the ninety basis points on the five-year, thirty basis points on a one-year – those are medicated, pegged rates created by the Fed and which fast-money traders trade against as long as they are confident the Fed can keep the whole market rigged. Nobody in their right mind wants to own the ten-year bond at a two percent interest rate. But they're doing it because they can borrow overnight money for free, ten basis points, put it on repo, collect 190 basis points a spread, and laugh all the way to the bank. And they will keep laughing all the way to the bank on Wall Street until they lose confidence in the Fed's ability to keep the yield curve pegged where it is today. If the bond ever starts falling in price, they unwind the carry trade. They unwind the repo, because then you can't collect 190 basis points.

Then you get a message, "Do not pass go." Sell your bonds, unwind your overnight debt, your repo positions. And the system then begins to contract – exactly what happened in September and October of 2008. Only, that time it was an unwind to the repo on mortgage-backed securities and CDOs and so forth. That was a minor trial run for the great unwind that is going to happen when the Treasury market is finally shattered with a lack of confidence because, on the margin, no one owns a Treasury bond: they just rent it on borrowed money. If the price starts falling, they'll get out of that trade as fast as they got out of toxic CDOs.

Alex: So when people run away from the US, they will run away all at once.

David: Well, if they run away from the Treasury, it sends compounding forces of contagion through the entire financial system. It hits next the MBS and the mortgage market. The mortgage market then scares the hell out of people about the housing recovery, which hasn't happened anyway. And if there isn't a housing recovery, middle-class Main-Street confidence isn't going to recover, because it is the only asset they have, and for 25 million households it's under water or close to under water.

Alex: We saw something much like that in 2008. All the markets correlated. Stocks went down. Bonds went down. Gold went down with them. It sounds like what you're saying is that the Fed is effectively paying bankers to stay confident in the Fed, and that the moment that stops – either because the Fed stops paying them or something else shakes their confidence – this all goes down in one big house of cards?

David: Yes, I think that's right. The Fed has destroyed the money market. It has destroyed the capital markets. They have something that you can see on the screen called an "interest rate." That isn't a market price of money or a market price of five-year debt capital. That is an administered price that the Fed has set and that every trader watches by the minute to make sure that he's still in a positive spread. And you can't have capitalism if the capital markets are dead, if the capital markets are simply a branch office – branch casino – of the central bank. That's essentially what we have today.

Alex: Last night you told our audience that if you were elected president, the first thing you would do is quit. Or at least demand a recount, I believe were your words, which I thought was telling. Are you saying there are no policy changes we could make today that would get us out of this? Or at least that wouldn't get you assassinated?

David: Yeah, there is a paper blueprint. People who believe in sound money and fiscal responsibility, that you create wealth the old-fashioned way through savings and work and effort and not simply by printing money and trading pieces of paper – there is a plan that they could put together. One would be to put the Fed out of business. You don't have to "end the Fed," although I like Ron Paul's phrase. You have to get them out of discretionary, active, day-to-day meddling in the money markets. Abolish the Open Market Committee.

The Fed has taken its balance sheet to $3 trillion. That's enough for the next 50 years. They don't have to do a damn thing except maybe have a discount window that floats above the market, and if things get tight, let the interest rate go up. People who have been speculating will be carried out on a stretcher. That's how they used to do it. It worked prior to 1914. That's the first step: abolish the Open Market Committee. Abolish discretionary monetary policy.

Let the Fed, if you're going to keep it – I don't even know that you need to do that, but if you are going to keep it – be only a standby source. As Badgett said (Walter Badgett, the great 19th-century British financial thinker): provide liquidity at a penalty rate to sound collateral.

Now, that's what J.P. Morgan did in 1907, in the great crisis of 1907, from his library. He didn't have a printing press. He didn't bail out everybody. He didn't do what Bernanke did and say: "Stop the presses, freeze everybody, and prop up Morgan Stanley and Goldman Sachs and all the rest of the speculators." The interest rate, the call-money interest rate, which was the open-market interest rate at the time, some days went to 30, 40, 70% – and they were carrying out the speculators left and right, liquidating margin debt, taking out the real estate speculators. Eight or ten railroads went bankrupt within a couple of months. The copper magnates got carried out on their shields.

This is the only way a capital market can work, but it needs an honest interest rate. And we have no interest rate, so therefore we solve nothing and we have the kind of impaired, incapacitated markets that we have today. They're very dangerous, because they're all dependent on twelve people. It is what I call "the monetary Politburo of the Western world," and they are just as dangerous as the Politburo in Beijing or the Politburo of memory in Moscow.

Alex: A twelve-person Open Market Committee determining the future of our economy by manipulating rates. Sounds like central planning to me.

David: It is. They are monetary central planners who are attempting to use the crude instrument of interest-rate pegging and yield-curve manipulation and essentially buying debt that no one else would buy, in order to keep this whole system afloat. It's Ponzi economics. Anybody who had financial training before 1970 would instantly recognize this as Ponzi economics. It is only because of the last twenty years we got so inured to prosperity out of the end of a printing press and massive incremental debt that people lost sight of the fundamental principles of sound money, which, there's nothing arcane about it. It's just common sense. It is not common sense to think that 50, 60, 70% of all the debt that's being created by the federal government can be bought by the Federal Reserve, stuffed in a vault, and everybody can live happily ever after.

Alex: So the government has certainly put us in a precarious position, but I don't think they alone have put America in this position, have they? You mentioned consumer debt becoming a major burden on the economy. How do we shed ourselves of that? I mean, the federal government can repudiate its debts if we walk away from it. We might see a few wars or something from that. It could inflate its way out of it. It can tax its way out of it. But how do households get out from under the debt burden that they have today?

David: Well, it's very tough, and they were lured into it by bad monetary policy when Greenspan panicked in December 2000. The interest rate was 6.5%; we had an economy that was threatened by competitors around the world. We needed high interest rates, not low. He panicked after the dot-com crash, and as you remember in two years they took the interest rate all the way down to 1%, and they catalyzed an explosion of mortgage borrowing, which was crazy.

When they cut the final rate down to 1% in May, June 2003, in that quarter – the second quarter of 2003 – the run rate of mortgage borrowing was $5 trillion at an annual rate. That was nuts! There had never been even a trillion-dollar annual rate of mortgage borrowing previously. In that quarter the run rate was $5 trillion, 40% of GDP. Why? Because the Fed took the rate down to 1%. Floating-rate product got invented everywhere. Anybody that had a pulse was being given mortgage loans by the brokers. The mortgage brokers didn't have any capital or funding. They went to Wall Street. They got warehouse lines, and the whole thing got out of control. Millions of households were lured into taking on debt that was insane, and now we have a generation of debt slaves.

There are 25 million households in America who couldn't move if they wanted to, because their mortgages are under water. They cannot generate a down payment and the 5% or 6% broker fee that you need to move. So we've got 25 million households immobilized, paralyzed, and worried every day about when they are going to lose property, because of what the Fed did. It's a terrible indictment.

Alex: Mobility itself is the American dream, isn't it? It's the ability to pick up and find work and then move and do all that. So now we have people who are slaves to their debt. How do we get ourselves out of this? Is this just a matter of personal financial discipline? Is there a policy move that can happen?

David: It's policy. If we don't do something about the Fed, if we don't drive the Bernankes and the Dudleys and the Yellens and the rest of these lunatic money-printers out of the Federal Reserve and get it under the control of people who have at least a modicum of sanity, we are just going to bury everybody deeper.

It's unfortunate. The American people are as much a victim of the Fed's massive errors as anything else. People were not prudent when they took on debt at 100% of the peak value of their property at some moment in 2004 and 2005. They were lured into it. But now we're stuck with something that didn't need to happen.

Alex: The Federal Reserve was founded in 1914, and it saw America through World War I, World War II. It saw America through Vietnam, saw America through the biggest boom in the economic history of the world. Yet now, today, you are calling for the abolishment of the Fed. Wasn't the Fed here the entire time that America was a prosperous, growing, wealthy, technology-driven nation? What's changed?

David: The greatest period of growth in American history was 1870-1914 – the Fed didn't exist. Right after 1870, when we recovered from the Civil War we went back on the gold standard. It worked pretty well. World War I was a catastrophe for the financial system. The Fed financed it, but I don't give them any credit for that, okay? We shouldn't have been in that war. It was a stupid thing to get involved in. But once we got involved in it, the Fed printed money like crazy, it facilitated borrowing, set the groundwork for the boom of the 1920s and the collapse of the 1930s.

Even then though, we had great minds who coped with reality in a pragmatic way in the Fed. Even Marriner Eccles wasn't all that bad. He stood up to Truman in 1951, when Truman wanted to force the Fed to continue to peg interest rates at 2% or 2.5% when inflation was 5%. Then we had William McChesney Martin: brilliant, pragmatic. He wasn't some kind of gold-standard guy in a pure sense, but a pragmatic guy who understood that prosperity had to come out of private productivity, out of investment, out of risk-taking, and the Fed had to be very careful not to allow speculation to start or inflation to get ignited. In 1958, he invented the phrase, "The job of the Fed is to take the punchbowl away." And we had a small recession. Six months after the recession was over he was actually raising the margin rate on the stock-market loans in order to quell speculation, and raising interest rates so that the economy didn't start to inflate again.

Now that was the regime we had until, unfortunately, Lyndon Johnson came along with his "guns and butter," took William McChesney Martin down to the ranch, and beat the hell out of him and forced him to capitulate. But here's the point I would make: In 1960, at the peak of what I call the golden era – the twilight of fiscal and financial discipline – we had $30 billion on the balance sheet of the Fed. It had taken 45 years to build that up. Then, as they began to rapidly expand the balance sheet of the Fed during the inflation of the '70s and the '80s, even then it took us until September 2008 – the Lehman collapse – to get to $900 billion. Had the balance sheet only grown at 3%, which is what the capacity of the economy to grow, I think, really is, it would have been $300 billion, so they were overshooting.

Alex: We're three times where we should be.

David: Where we should have been by the Lehman crisis event. In the next seven weeks, this crazy lunatic who's running the Fed increased the balance sheet of the Fed by $900 billion, in seven weeks. In other words, they expanded the balance sheet of the Fed as rapidly in seven weeks as it had occurred during the first 93 years of its existence. And that's not all, as they say on late night TV: in the next six weeks they added another $900 billion. So in thirteen weeks they tripled the balance sheet of the Fed.

Alex: Wow, that's an incredible…

David: So no wonder we are in totally uncharted waters, and it's being run by people who are clueless as to how to get out of the corner they've painted this country into. They really ought to be run out of town on a rail.

Alex: I think you'd find that a lot of our viewers would agree with you on that one. You know, the average American is suffering. It looks like the average American is going to have to suffer more to get us out of this, but it seems like the only thing the Fed is interested in these days is propping up the stock market. Why is that? Where does that come from?

David: The Fed has taken itself hostage with this whole misbegotten doctrine of wealth effects, which was created by Greenspan. In other words, if we get the stock market going up and we get the stock averages going up, people feel wealthier, they will spend more. If they spend more, there is more production and income and you get a virtuous circle. Well, that says you can create wealth through speculation. That can't be true, because if it is true, we should have had a totally different kind of system than we've had historically.

So they got into that game, and then the crisis came in September, 2008. They panicked and pulled out the stops everywhere. As I said, tripled the balance sheet in thirteen weeks, [compared to what] they had done in 93 years. They are now at a point where they don't dare begin to reduce the balance sheet, begin to contract, or they'll cause Wall Street to go into a hissy fit. They are afraid to death of Wall Street going into a hissy fit, so essentially, the robots and the boys and girls and the fast-money traders on Wall Street run the Fed indirectly.

Alex: So, in the 1960s, the Fed is taking away the punchbowl. Sounds like in 2010 the Fed is the one adding the alcohol. They are afraid to stop, lest everybody riot.

David: Yes, they got the party going, and they're afraid to stop it. As a result of that you have a doomsday machine.

Alex: At some point we are going to be forced to stop. Market forces will kick in and Europe and China and India will stop lending us money.

David: Yes. As I say, when the crisis comes in the Treasury market, it will be the great margin call in the sky. They'll start unwinding all of the carry trades, all of the repo. Asset prices generally will be affected, because this will ricochet and compound through the system.

Alex: When does this happen?

David: People looked at the housing market and the mortgage market way back in 2003 – there were some smart people looking at this. They looked at the run rate of gross mortgage issuance, the $5 trillion I was talking about, and said: "This is insane, this is off the charts, this is so far beyond anything that has ever happened before, something bad is going to come of this." It's obvious, if you pour debt into markets… I mean a lot of people leveraged 98%, or whatever they were doing at the time with so-called mortgage insurance, and just high loan to value ratios. They were driving up prices, and so there was a housing-price boom going on. It was sucking the whole middle class into speculation. So that's the nature of the system, and now they don't know how to unwind it.

Alex: That's a pretty stark picture. So as an individual investor, what are we to do? How do we protect ourselves in this type of situation? Should I be owning bonds and staying out of stocks? Should I be owning stocks?

David: No, I would stay out of any security markets. These are unsafe markets at any speed. It's all tied together. As I was saying when the great margin call comes and they start selling the Treasury bond, they'll take everything else with it. Real estate is priced off Treasuries. Mortgaged-backed securities are priced off Treasuries. Corporates are priced off Treasuries. Junk bonds are priced off Treasuries. Everything. The stock market will go into a panic. We don't know when the timing will come – we've never been in a world where there is $15 trillion worth of central-bank balance sheets, like we have today. The only thing I think you can conclude is preservation is the only thing you are about as an investor. Forget about yield. Forget about return. Just keep yourself liquid and preserve your capital, because you can't predict the day when, as I say, the great margin call in the sky comes down.

Alex: So if it's not about coming out ahead, it's about coming out not behind everybody else. It's just losing a little less. What's the most effective way to do that? Do you want to hold cash? Alternative options?

David: Yes. I don't even think there's nothing wrong with owning Treasury bills. I mean, if you want to get, for a one-year Treasury, what is the thing now? Twenty basis points or something?

Alex: So when the great Treasury crash comes, I should own Treasury bills?

David: Well, it doesn't mean the price of the Treasury is going to crash, no.

Alex: Okay, so we are just going to see interest rates skyrocket on new issues. The US government is not going to be able to borrow.

David: That's why you're short. If you're in a thirty-day piece of paper, you're not going to lose principal.

Alex: What happens to the dollar in all of this? If I'm holding dollar denominated assets –?

David: Well, the dollar, in theory, people would think is going to crash. I don't think it is because all the rest of the currencies in the world are worse.

Alex: So once again, America is not that bad off.

David: Well, we're bad off because when the financial markets reprice drastically, it's going to have a shocking effect on economic activity. It's going to paralyze things. It's going to finally cause consumption to come down. It's going to cause government spending to be retracted.

You know, the Keynesians are right. Borrowing does add to GDP accounts. But it doesn't add to wealth. It doesn't add to real productivity, but it does add to GDP as it's calculated and published – because GDP accounts were designed by Keynesians who don't believe in a balance sheet. So they said, "If the public sector and the household sector are borrowing, let's say, $10 trillion next year, run it though GDP, you'll get a big bump to GDP." But sooner or later your balance sheet will collapse. They forgot about that one. So my point is that we've gone through a thirty-year expansion of the balance sheet, an artificial growth in GDP; now we're going to have to be retracting the collective balance sheets. That means that GDP will not grow. It may even contract, and no one's prepared for that.

Alex: So the economy will collapse. The dollar will be okay, because we still need a medium of exchange and the dollar is the least-bad currency in the world. How does gold fit into the picture? Do you think that gold is a good asset?

David: Yes, I think that gold is a good asset. It's the only currency that anybody is going to believe in after a while.

Alex: Okay, so maybe hold that as an insurance policy. Do you own gold yourself?

David: Yes, as an insurance policy.

Alex: Where else do you invest in today?

David: I'm preserving capital. I'm in cash. I don't think the risk of the system is worth it.

Alex: So you are practicing what you preach, 100%?

David: Yes.

Alex: That's great. It's good to hear. This is excellent advice for our subscribers as well, to consider that there's a lot of potential energy built up in the system. You've articulated it well, a lot of painful policy moves ahead of us, and probably something that makes 2008 look like a preview, if you will.

David: It was just a warm-up.

Alex: Just a warm-up. Thank you very much.

David: Thank you.

A selected excerpt by David Stockman from his just released interview with Alex Daley of Casey Research:

This market isn't real. The two percent on the ten-year, the ninety basis points on the five-year, thirty basis points on a one-year – those are medicated, pegged rates created by the Fed and which fast-money traders trade against as long as they are confident the Fed can keep the whole market rigged. Nobody in their right mind wants to own the ten-year bond at a two percent interest rate. But they're doing it because they can borrow overnight money for free, ten basis points, put it on repo, collect 190 basis points a spread, and laugh all the way to the bank. And they will keep laughing all the way to the bank on Wall Street until they lose confidence in the Fed's ability to keep the yield curve pegged where it is today. If the bond ever starts falling in price, they unwind the carry trade. Then you get a message, "Do not pass go." Sell your bonds, unwind your overnight debt, your repo positions. And the system then begins to contract... The Fed has destroyed the money market. It has destroyed the capital markets. They have something that you can see on the screen called an "interest rate." That isn't a market price of money or a market price of five-year debt capital. That is an administered price that the Fed has set and that every trader watches by the minute to make sure that he's still in a positive spread. And you can't have capitalism if the capital markets are dead, if the capital markets are simply a branch office – branch casino – of the central bank. That's essentially what we have today.From Casey Research

The New Economic Collapse Video: It makes uncomfortable but urgent viewing.

When Casey Research Chief Technology Investment Analyst Alex Daley met former Reagan Budget Director David Stockman to talk about the economy and where he sees it leading taxpayers investors and savers in the near future, he got some very intriguing insights from a man who served right at the heart of the US federal government.

True, some if it makes for uncomfortable watching, but the message is critical if you want to keep your assets safe in what David calls calls "the great unwind."

Watch the video and secure your money.

Full Transcript:

Interviewed by Alex Daley, Chief Technology Investment Strategist, Casey Research

Alex Daley: Hello. I'm Alex Daley. Welcome to another edition of Conversations with Casey. Today our guest is former Reagan Budget Director and Congressman David Stockman. Welcome to the show, David.

David Stockman: Glad to be here.

Alex: So we're here in Florida talking at the Recovery Reality Check Casey Summit. What do you think: is the United States economy on the road to recovery?

David: I don't think we are at the beginning of the recovery. I think we are at the end of a disastrous debt supercycle that has gone on for the last thirty or forty years, really. It started when Nixon defaulted on our obligations under Bretton Woods and closed the gold window. Incrementally, year after year since then, we have been going in a direction of extremely unsound money, of massive borrowing in both the private and the public sector. We now have an economy that is saturated with debt: $54 trillion or $53 trillion – 3.5 times the GDP – way off the charts from where it was for a hundred years prior to the beginning of this. The idea that somehow all of that debt is irrelevant, as the Keynesians would tell us, is fundamentally wrong – and the reason why the economy can't get up off the mat.

We're doing all the wrong things. We're adding to the problem, not subtracting. We are not allowing the debt to be worked down and liquidated. We're not asking people to save more and consume less, which is what we really need to do. And so therefore I think policy is just making it worse, and any day now we will have another recurrence of the kind of economic crisis we had a few years ago.

Alex: You paint a very stark picture, but if people just stop spending, start saving, won't companies like Apple see their earnings hurt? Won't the stock market then start to tumble, people's net worth fall? Isn't that a negative cycle that feeds on itself?

David: Sure it does, but you can't live beyond your means because it's pleasant. It's not sustainable. Clearly the level of debt that we have is not sustainable. We have a whole generation – the Baby Boom – that's about ready to retire, and they have no retirement savings. We have a federal government that is bankrupt, literally. Its [debt is] $16 trillion and growing by a trillion a year. Something's going to give. We can't pay for all these entitlements. There won't be the revenue generation in the economy to do it.

So as a result of that, we are deluding ourselves if we think we can just continue to spend. Look at the GDP that came out in the first quarter of this year. It was only 2.2%. Most of it was personal consumption expenditure, and half of that was due to a drawdown of the savings rate, not because the economy was earning more income or generating more real output. It was because of a drawdown of savings. That is exactly the wrong way to go – an indication of how severe the crisis is going to be.

I'm not saying the economy should stop spending entirely. I'm only saying you can't save 3% of GDP and spend 97% if you are going to get out of this fix. As the savings rate goes up both in the public sector (which means reduction of spending and the deficit) and the household sector (to seriously reduce debt burden, which has not really happened) we are going to, on the margin, spend less, save more. It will slow down the economy. It will undermine profits, I agree. But profits today are way overstated. They're based on a debt-bloated economy that isn't sustainable.

Alex: So we can only live beyond our means for so long, as any family knows.

David: Yes.

Alex: Now, the government can reduce its expenses at any time by simply reducing spending, and it can reduce debt if it brings in more tax revenue. That's austerity – I think that's how they refer to it. But won't austerity cause massive joblessness? Won't there be millions more people in this country not receiving a paycheck?

David: Yes, but the critique, the clamoring and clattering that you hear from the Keynesians (or even mainstream media, which is pretty clueless economically) that austerity is bad forgets the fact that austerity isn't an elective course. Austerity is something that happens to you when you're broke. And yes, it is painful and spending will go down and unemployment will go up and incomes will be impaired, but that is a consequence of the excess debt creation that we've had for the last thirty years. So austerity is what happens when you break the rules.

And somehow we have this debate going on. They're making a mistake. They chose the wrong strategy. Do you think Greece chose the wrong strategy with austerity? No. No one would lend them money. That's why they ended up in the place they were. Do you think that Spain today is teetering on the brink because they said, "Oh, wouldn't it be a good idea to have austerity?" No, they had a gun to their head. They were forced to do this because the markets would not continue to lend, and even now their interest rate is again rising. The markets are losing confidence, and unless the ECB prints some more money and bails them out some more, they are going to have austerity. So the austerity upon us is the backside of the debt supercycle we had for the past thirty years. It's not discretionary.

Alex: Austerity hasn't been forced upon us yet. The dollar is up, people are continuing to buy Treasuries – both nations and banks are buying Treasuries. To all extents and purposes, people are continuing to show massive confidence in the US government, lend it money at extremely cheap interest rates, and letting it build up its debt.

So you are advocating that, unlike Greece or Spain taking it to the edge and having austerity forced on them, we should volunteer for austerity today? Instead of just kicking the can down the road and living high a little bit longer, until the bill collectors finally come knocking? Why go today, why start austerity now instead of doing what Greece did and going as long as you possibly can?

David: Because Greece is a $300 billion economy. Tiny. A rounding error in the great scheme of things. It's – last time I checked – about eight and a half months' worth of Walmart sales. Okay? That's a little different than when you have the $15 trillion heartland of the world economy, and the $11 trillion Treasury market which is at the center of the whole global financial system buckle and falter. That's the risk you're taking if you say, "Mañana. Kick the can; let's just wait for something good to happen."

This market isn't real. The two percent on the ten-year, the ninety basis points on the five-year, thirty basis points on a one-year – those are medicated, pegged rates created by the Fed and which fast-money traders trade against as long as they are confident the Fed can keep the whole market rigged. Nobody in their right mind wants to own the ten-year bond at a two percent interest rate. But they're doing it because they can borrow overnight money for free, ten basis points, put it on repo, collect 190 basis points a spread, and laugh all the way to the bank. And they will keep laughing all the way to the bank on Wall Street until they lose confidence in the Fed's ability to keep the yield curve pegged where it is today. If the bond ever starts falling in price, they unwind the carry trade. They unwind the repo, because then you can't collect 190 basis points.

Then you get a message, "Do not pass go." Sell your bonds, unwind your overnight debt, your repo positions. And the system then begins to contract – exactly what happened in September and October of 2008. Only, that time it was an unwind to the repo on mortgage-backed securities and CDOs and so forth. That was a minor trial run for the great unwind that is going to happen when the Treasury market is finally shattered with a lack of confidence because, on the margin, no one owns a Treasury bond: they just rent it on borrowed money. If the price starts falling, they'll get out of that trade as fast as they got out of toxic CDOs.

Alex: So when people run away from the US, they will run away all at once.

David: Well, if they run away from the Treasury, it sends compounding forces of contagion through the entire financial system. It hits next the MBS and the mortgage market. The mortgage market then scares the hell out of people about the housing recovery, which hasn't happened anyway. And if there isn't a housing recovery, middle-class Main-Street confidence isn't going to recover, because it is the only asset they have, and for 25 million households it's under water or close to under water.

Alex: We saw something much like that in 2008. All the markets correlated. Stocks went down. Bonds went down. Gold went down with them. It sounds like what you're saying is that the Fed is effectively paying bankers to stay confident in the Fed, and that the moment that stops – either because the Fed stops paying them or something else shakes their confidence – this all goes down in one big house of cards?

David: Yes, I think that's right. The Fed has destroyed the money market. It has destroyed the capital markets. They have something that you can see on the screen called an "interest rate." That isn't a market price of money or a market price of five-year debt capital. That is an administered price that the Fed has set and that every trader watches by the minute to make sure that he's still in a positive spread. And you can't have capitalism if the capital markets are dead, if the capital markets are simply a branch office – branch casino – of the central bank. That's essentially what we have today.

Alex: Last night you told our audience that if you were elected president, the first thing you would do is quit. Or at least demand a recount, I believe were your words, which I thought was telling. Are you saying there are no policy changes we could make today that would get us out of this? Or at least that wouldn't get you assassinated?

David: Yeah, there is a paper blueprint. People who believe in sound money and fiscal responsibility, that you create wealth the old-fashioned way through savings and work and effort and not simply by printing money and trading pieces of paper – there is a plan that they could put together. One would be to put the Fed out of business. You don't have to "end the Fed," although I like Ron Paul's phrase. You have to get them out of discretionary, active, day-to-day meddling in the money markets. Abolish the Open Market Committee.

The Fed has taken its balance sheet to $3 trillion. That's enough for the next 50 years. They don't have to do a damn thing except maybe have a discount window that floats above the market, and if things get tight, let the interest rate go up. People who have been speculating will be carried out on a stretcher. That's how they used to do it. It worked prior to 1914. That's the first step: abolish the Open Market Committee. Abolish discretionary monetary policy.

Let the Fed, if you're going to keep it – I don't even know that you need to do that, but if you are going to keep it – be only a standby source. As Badgett said (Walter Badgett, the great 19th-century British financial thinker): provide liquidity at a penalty rate to sound collateral.

Now, that's what J.P. Morgan did in 1907, in the great crisis of 1907, from his library. He didn't have a printing press. He didn't bail out everybody. He didn't do what Bernanke did and say: "Stop the presses, freeze everybody, and prop up Morgan Stanley and Goldman Sachs and all the rest of the speculators." The interest rate, the call-money interest rate, which was the open-market interest rate at the time, some days went to 30, 40, 70% – and they were carrying out the speculators left and right, liquidating margin debt, taking out the real estate speculators. Eight or ten railroads went bankrupt within a couple of months. The copper magnates got carried out on their shields.

This is the only way a capital market can work, but it needs an honest interest rate. And we have no interest rate, so therefore we solve nothing and we have the kind of impaired, incapacitated markets that we have today. They're very dangerous, because they're all dependent on twelve people. It is what I call "the monetary Politburo of the Western world," and they are just as dangerous as the Politburo in Beijing or the Politburo of memory in Moscow.

Alex: A twelve-person Open Market Committee determining the future of our economy by manipulating rates. Sounds like central planning to me.

David: It is. They are monetary central planners who are attempting to use the crude instrument of interest-rate pegging and yield-curve manipulation and essentially buying debt that no one else would buy, in order to keep this whole system afloat. It's Ponzi economics. Anybody who had financial training before 1970 would instantly recognize this as Ponzi economics. It is only because of the last twenty years we got so inured to prosperity out of the end of a printing press and massive incremental debt that people lost sight of the fundamental principles of sound money, which, there's nothing arcane about it. It's just common sense. It is not common sense to think that 50, 60, 70% of all the debt that's being created by the federal government can be bought by the Federal Reserve, stuffed in a vault, and everybody can live happily ever after.