How Warren Buffett is Different from Most Investors, Part 1:

There was an academic article published recently on the investing of Warren Buffett. Afterward, I thought I saw a few articles reflecting on it, but here is the only one I see now: There’s Warren Buffett — and then there’s the rest of us.

Buffett is different, because he grew as an investor and as a businessman, and usually made the right moves over a 50+ year career. When you don’t have a lot of assets, and few people are doing value investing, you can do amazing things with special situations, and being an activist investor. In 1967, Buffett had control of a textile company named Berkshire Hathaway, when he used the resources of the company to purchase some smallish P&C insurance companies, National Indemnity and National Fire and Marine Insurance.

This brings up the first way that Buffett is different than most investors. He understands and invests in a complex industry, P&C insurance. He begins to realize that it can be used as a platform for greater investing. As he sees that potential, he buys half of GEICO in the 70s, before buying the whole company in 1994.

This brings up the second way that Buffett is different than most investors: Buffett was willing to buy whole companies, not replace management for the most part, and operate them. Buffett limited himself to being the wholly-owned company’s board, asking questions on management competence, and redirecting free cash flow for the greater good of Berkshire Hathaway.

That brings me to the third way in which Buffett is different than most investors: He analyzes cash flow streams from investments, and buys shares in companies, or the whole company when they offer a reliable high prospective free cash flow yield. And it brings me to the fourth way Warren Buffett is different than most investors: Buffett does not diversify, particularly in the early years. He plays for best advantage. Buffett views investing through the lens of compounding cash flows, and does not pay much attention to the market as a whole.

In my opinion, it is a worthy use of time (but don’t neglect your family) to read through the annual letters of Berkshire Hathaway. If you do that, you will get a sense of a clever businessman who would invest for best advantage. His tactics shifted over time, but he was always looking to compound free cash flows at the best possible rate.

I’m going to hit the publish button now, but I will finish this in part 2.

Sunday, August 26, 2012

Saturday, August 18, 2012

The Slowing De-leveraging….

The Slowing De-leveraging….:

I’ve long predicted that the balance sheet recession was likely to come to an end somewhere around 2013/2014 and it looks like the de-leveraging process in the USA has certainly slowed. This excellent chart from Morgan Stanley (via Joe W) shows how the de-leveraging has improved over the years. Unfortunately, we’re not quite at a point where the public sector can hand off the baton yet. We still have some work to do so we’re likely looking at something closer to a 2014 hand-off of the baton. Of course, that’s assuming the fiscal cliff doesn’t torpedo the private sector recovery right when it looks like it’s starting to catch its footing….

I’ve long predicted that the balance sheet recession was likely to come to an end somewhere around 2013/2014 and it looks like the de-leveraging process in the USA has certainly slowed. This excellent chart from Morgan Stanley (via Joe W) shows how the de-leveraging has improved over the years. Unfortunately, we’re not quite at a point where the public sector can hand off the baton yet. We still have some work to do so we’re likely looking at something closer to a 2014 hand-off of the baton. Of course, that’s assuming the fiscal cliff doesn’t torpedo the private sector recovery right when it looks like it’s starting to catch its footing….

Source: Morgan Stanley via Joe Weisenthal

Monday, August 13, 2012

Gary Shilling: US in Recession Now or Within 3 Months, Deleveraging Will Take 5-7 More Years

Gary Shilling: US in Recession Now or Within 3 Months, Deleveraging Will Take 5-7 More Years: In a Daily Ticker Interview with Henry Blodget, economist Gary Shilling makes the case the US is already in recession.

On June 21, I made the case 12 Reasons US Recession Has Arrived (Or Will Shortly)

On July 11, I wrote Case for US and Global Recession Right Here, Right Now; Recognizing the Limits of Madness; Permabears?

More QE is Pointless

While everyone is looking for another round of QE, on August 1, I explained Another Round of QE is Pointless.

Shilling thinks the recession started in the second quarter. Obviously, I agree.

It will be interesting to see when and where the NBER places it.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

"We've had three consecutive months of declines in retail sales," says Shilling, president of A. Shilling & Co., an economic research and forecasting firm. "That's happened 29 times since they started collecting the data in 1947, and in 27 of the 29 we were either in a recession or within three months of it."Case for Recession

Shilling expects this recession will last about a year and shave about 3.5% from growth from peak to trough.

This time is different, says Shilling "because a lot of things that normally go down in a recession are already there, like housing." And policies that normally help revive the economy are absent. The Fed can't cut interest rates because they're already near zero and the housing market won't be a catalyst for growth, Shilling says.

Before the last presidential election Shilling said that whoever got elected then wouldn't get re-elected because the economy would still be weak with high unemployment.

Now Shilling says he'd like to see one party in control in Washington because it increases the odds of cuts for entitlements and could help "restore confidence in Washington." But even then he says it will take five to seven years to complete the deleveraging that's already underway before the economy recovers.

On June 21, I made the case 12 Reasons US Recession Has Arrived (Or Will Shortly)

On July 11, I wrote Case for US and Global Recession Right Here, Right Now; Recognizing the Limits of Madness; Permabears?

More QE is Pointless

While everyone is looking for another round of QE, on August 1, I explained Another Round of QE is Pointless.

Would Another Round of QE Help?Timing the Recession

Everyone is looking for the Fed to do something.

I have to ask what good could it possibly do? Yield on the 10-year

treasury is about 1.5%. Would it make any difference to businesses if it

was 1.25% or even 1%?

I suggest additional monetary stimulus would not do anything to spur job

creation and it would continue to punish those on fixed incomes.

An additional round of QE could ignite a further rally in equities

(already in bubble land). However, one of these QE moves by the Fed will

blow sky high, and with equities priced beyond perfection, the next

round of QE may be the one.

Shilling thinks the recession started in the second quarter. Obviously, I agree.

It will be interesting to see when and where the NBER places it.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

Tuesday, August 07, 2012

Guest Post: While All Eyes Are On Europe, Japan Circles A Black Hole

Guest Post: While All Eyes Are On Europe, Japan Circles A Black Hole:

Submitted by Charles Hugh-Smith of OfTwoMinds blog,

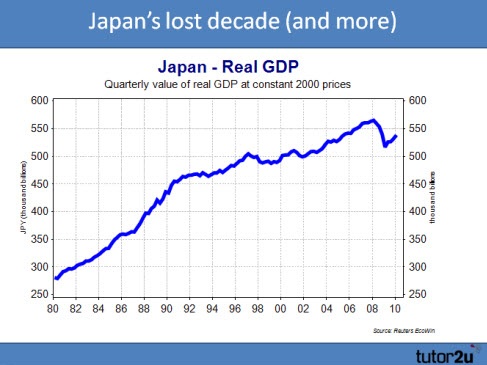

While all eyes are on the absurdist tragicomedy playing out in Europe, Japan is quietly circling a financial black hole as its export economy is destroyed by its strong currency and the global recession.

There is a terrible irony in export-dependent nations being viewed as "safe havens." Their safe haven status pushes their currencies higher, which then crushes their export sector, which then weakens their entire economy and stability, undermining the very factors that created their safe haven status.

As long as Germany stays within the Eurozone, Japan is the primary example of this dynamic. Should Germany leave the euro and return to its own currency, it too will begin orbiting the financial black hole of declining exports driven by a strengthening currency in a global recession.

Economies that are less reliant on exports are much less exposed to the consequences of a strengthening currency.

We can lay out the dynamic of Japan's currency and export-dependent economy thusly:

1. Export-dependent economies such as Japan, China and Germany rely on strong exports to sustain their employment and growth.

2. This means they must maintain positive current accounts (trade surpluses).

3. As their currencies strengthen, their exports become less competitive globally.

4. Export-dependent economies must pursue strategies to keep their currencies aligned with their buyers, the importing nations.

5. Germany has done so via the eurozone, which aligned its largest import market, Europe, with its own currency.

6. China has done so by pegging the renminbi (yuan) to the U.S. dollar and restricting foreign exchange (i.e. not allowing a free-floating renminbi).

7. Japan has neither of these advantages, and must intervene in the FX markets by buying and selling yen and dollars.

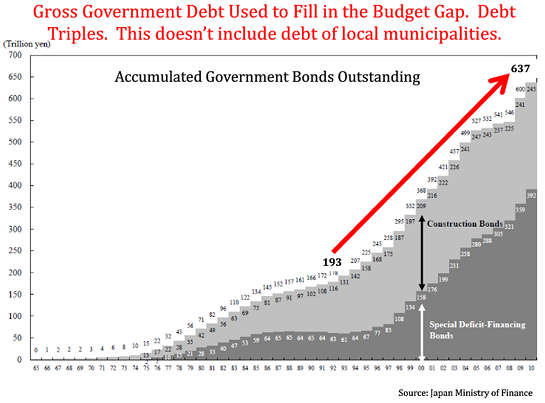

8. Despite its well-known debt problems (see chart below), Japan retains a massive and diverse industrial base, a current-account surplus (or modest deficit with its nuclear power plants largely offline) and large overseas assets.

9. These assets, plus its homogeneous culture, makes Japan an island of stability in an increasingly unstable global economy.

10. For these reasons, the yen is considered a "safe haven" currency and yen-denominated bonds as "safe haven" liquid investments.

11. As demand for yen rises, the currency strengthens, weakening the competitiveness of Japanese exports.

12. The "safe haven" status of the yen ends up hurting the Japanese economy's primary engine, exports.

13. The stronger yen ends up weakening the very attributes that make the yen and Japanese bonds "safe havens."

14. As the global economy slides into recession, exports decline sharply under the double-whammy of falling demand and a rising currency.

Ironic, to say the least.

Submitted by Charles Hugh-Smith of OfTwoMinds blog,

While all eyes are on the absurdist tragicomedy playing out in Europe, Japan is quietly circling a financial black hole as its export economy is destroyed by its strong currency and the global recession.

There is a terrible irony in export-dependent nations being viewed as "safe havens." Their safe haven status pushes their currencies higher, which then crushes their export sector, which then weakens their entire economy and stability, undermining the very factors that created their safe haven status.

As long as Germany stays within the Eurozone, Japan is the primary example of this dynamic. Should Germany leave the euro and return to its own currency, it too will begin orbiting the financial black hole of declining exports driven by a strengthening currency in a global recession.

Economies that are less reliant on exports are much less exposed to the consequences of a strengthening currency.

We can lay out the dynamic of Japan's currency and export-dependent economy thusly:

1. Export-dependent economies such as Japan, China and Germany rely on strong exports to sustain their employment and growth.

2. This means they must maintain positive current accounts (trade surpluses).

3. As their currencies strengthen, their exports become less competitive globally.

4. Export-dependent economies must pursue strategies to keep their currencies aligned with their buyers, the importing nations.

5. Germany has done so via the eurozone, which aligned its largest import market, Europe, with its own currency.

6. China has done so by pegging the renminbi (yuan) to the U.S. dollar and restricting foreign exchange (i.e. not allowing a free-floating renminbi).

7. Japan has neither of these advantages, and must intervene in the FX markets by buying and selling yen and dollars.

8. Despite its well-known debt problems (see chart below), Japan retains a massive and diverse industrial base, a current-account surplus (or modest deficit with its nuclear power plants largely offline) and large overseas assets.

9. These assets, plus its homogeneous culture, makes Japan an island of stability in an increasingly unstable global economy.

10. For these reasons, the yen is considered a "safe haven" currency and yen-denominated bonds as "safe haven" liquid investments.

11. As demand for yen rises, the currency strengthens, weakening the competitiveness of Japanese exports.

12. The "safe haven" status of the yen ends up hurting the Japanese economy's primary engine, exports.

13. The stronger yen ends up weakening the very attributes that make the yen and Japanese bonds "safe havens."

14. As the global economy slides into recession, exports decline sharply under the double-whammy of falling demand and a rising currency.

Ironic, to say the least.

Subscribe to:

Posts (Atom)